David's Data- Jetcon : The Used Car Dealership

Hello, everyone! Here’s the latest installment of David’s Data, where he gives a comprehensive analysis of Jetcon Corporation Limited. Leave any feedback you have in the comments below or you can send them directly to David at his Twitter account or at our own Twitter or e-mail. Enjoy!

-The EveryMickle Team

Jetcon: The Used Car Dealer

In the space of car sales, there are two main segments one can think of for personal vehicle ownership. The new cars are often represented by the Porsche’s, Benz, Jaguar and BMW brands while the used cars are often represented by a wide cross section of brands ranging from Honda’s Nissan’s, Toyota’s, Mazada’s and many others. The new car sales are carried by a brand dealer who operates in a higher net worth segment while the used car sales are represented by independent dealers who operate their respective car lots trying to sway the regular consumer to purchase their vehicles. In this space, one can think of several dealers such as AutoChannel, Carland, Prospective Motors and Superior Parts Limited. However, today’s article will focus on the only company to take the step of public equity which is Jetcon Corporation Limited.

“The company, which was started by Andrew Jackson in 1994, has grown from a small dealer representing a couple million dollars in sales to a firm leading to the tune of $1 Billion in annual sales”

The company, which was started by Andrew Jackson in 1994, has grown from a small dealer representing a couple million dollars in sales to a firm leading to the tune of $1 Billion in annual sales. Spurred by the birth of his twins, Andrew started this company and continuously reinvested to allow for the company to scale up and compete in Jamaica’s growing auto market. With John Jackson as the lead (Chairman), his company went public in under a span of 3 months just before the stipulated timeline the government of Jamaica had anticipated to end the junior market benefits. This saw the company raise $88 Million which went towards working capital (current assets-current liabilities) and allow for the acquisition of a bonded warehouse to allow for them to keep a larger inventory of vehicles.

Since the IPO, the company has managed to surpass the $1 Billion mark for the last 3 Financial Years (FY) in annual sales and also bring in a minimum of $60 Million in net profit yearly while simultaneously paying $13 Million plus worth of dividends. This has been supported by consistent marketing and greater exposure through being listed on the Jamaica Stock Exchange. As the economy begins to soften again and the market looks dim, let’s review the company and its moves.

Financial Analysis

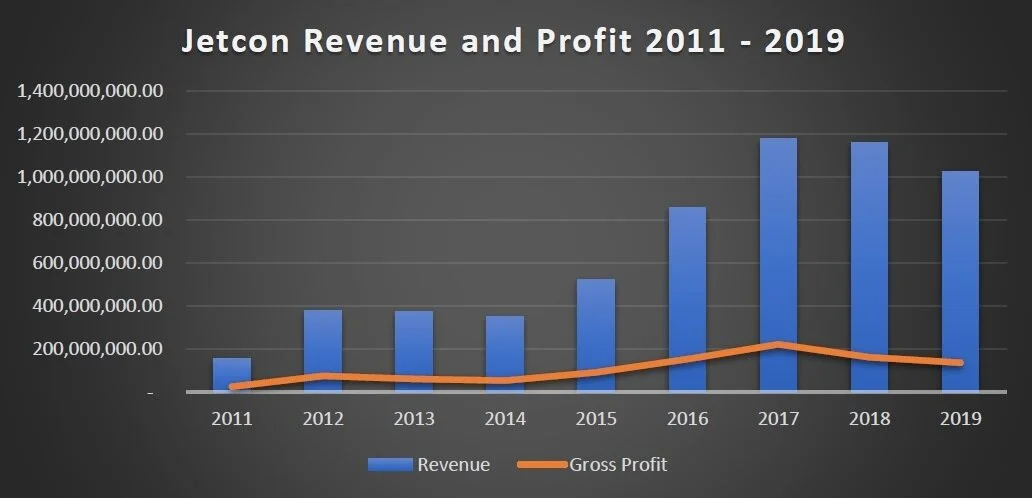

Jetcon has managed to grow revenues from $155.6 Million in 2011 to $1.02 Billion in 2019. This increase came mainly from greater space to store inventory ahead of client requests along with growing import demand for cars in Jamaica. This demand led to the eventual expansion of several thoroughfares in Kingston and St. Catherine to facilitate the growing population, which also bought more cars. However, this increased revenue has not translated to greater gross profits which have somewhat been stifled as costs have gone up over the years. At the peak year of revenues in 2017, gross profit grew to $221.7 Million, a 19% gross profit margin. In the two most recent Financial Years, the gross profit margin was at an average 14% which represents the narrow band in which the company operates on.

Operating expenses and financing costs have risen at a similar rate with respect to revenues which represent the associated costs to run the business. The good thing is that the company has less than 40 employees and has only garnered greater expenses associated with security and leasing costs for spaces they don’t own.

“For the years available and under review (2014 -2019), net profit has gone from a low of $10.5 Million to a peak of $153.8 Million in 2017”

For the years available and under review (2014 -2019), net profit has gone from a low of $10.5 Million to a peak of $153.8 Million in 2017. However, this peak year hasn’t been repeated with expenses eating away at what gross profit has been derived, with 2019 only recording a $60.3 Million net profit against $1.02 Billion in revenues. 2017 represented a 13% net profit margin while 2019 was a minor 6% net profit margin. These narrow margins show how fragile the company is to any gradual expense shifts while highlighting how beneficial the junior market has been, since they haven’t incurred the normal 25% corporate income tax rate over the last 3 years. Without this concession, the firm might have struggled to grow revenues any higher and might have possibly incurred losses.

Company Analysis

“The company serves mainly young entry level professionals who want a vehicle at the beginning of their careers”

Jetcon operates under a simple principle as it relates to selling their inventory. They work with 6 commercial banks to process the sale of vehicles to the customers who wants to purchase them. This purchase is usually financed by debt through that commercial bank. Jetcon is paid in the present by the bank whose client agrees to repay the bank in the future. Since Jetcon’s pricing segment is relatively competitive versus other dealers, it is easier to process clients through the commercial bank and arrange the processing of those vehicles. This segment as stated by Andrew Jackson represents 95% of the company’s revenue. As highlighted by the industry analysis, the company serves mainly young entry level professionals who want a vehicle at the beginning of their careers. In a country such as Jamaica which lacks an organized essential travel system, purchasing a vehicle is seen more of as a need to live rather than just for comfort. Listed company Knutsford Express Limited operates in the transport of people from different points of the island to the other in comfort and ease. However, the comparable Jamaica Urban Transit Company (JUTC) doesn’t serve the needs of those who want to travel across the capital and St. Catherine area since persons are limited by where the JUTC goes to and the time it takes to get there. As a result, many persons opt to get a vehicle rather than go through the struggle of getting public transport.

The company sources its vehicles from Japan which are usually refurbished with minimal incidents of damage. These vehicles are bought for a much cheaper price and sold back to the Jamaican market with a markup. The company is also engaged in the process of re-exportation to other Eastern Caribbean countries through its newly used Special Economic Zone (SEZ) warehouse space. The vehicles in question are cars, SUV’s, and small commercial vehicles with brands which range from Toyota, Mazda, Subaru, Mistubishi, Nissan and BMW’s.

The company also provides servicing for vehicles and spare parts for those who need them for their vehicles. While representing a small segment of revenues, it is still a great way to reengage customers and build new one’s through excellent service. With Jamaica’s numerous perils from pot holes, incomplete roads and the occasional damage from daily interactions, spare parts come in handy for those who need to get it replaced quickly and get on with their business.

Balance Sheet Analysis

The company’s total asset base has grown from $122.7 Million in 2014 to $680.7 Million in 2019. The majority of these assets are in the form of inventory which are the cars which remain with the firm. However, their cash base has been very minimal with the firm usually having less than $20 Million on hand at the end of any financial year. This reveals how much the company needs to generate sales in order for them to remain viable for the future.

The total liabilities of the company haven’t increased at that similar rate with liabilities being below $60 Million for most of the time excluding 2017 and 2019 when the company incurred debt and more payables on their side. However, this isn’t a bad thing since the company has never been over leveraged and has settled relationships with their vendors as needed. It remains a big risk for the firm though since their cash on hand is never enough to cover an immediate emergency without utilizing their bank overdraft facility. Over the past 10 years (2011-2019), the bank overdraft has usually been greater than the cash on hand. 2019 was the first financial year the company ended a period without the facility on their books.

Cash Flow Analysis

The company’s cash flow has been erratic over the last 10 years with cash flow from operations usually being well below net profits. 2013, 2016 and 2019 are the only years the company has been free cash flow (cash flow from operations – cash flow from investing) negative. This has been a unique case in the last financial year when considering they were reinvesting into the business heavily.

Cash flow from investing activities were smaller than $1 Million before 2017 seeing as the company never needed to invest heavily into that segment since they didn’t have the cash to support that initiative.

Cash flow from financing activities has mainly been negative excluding 2016 (IPO year) as the company secured loans for operations and only recently started to pay dividends in 2017. With the company entering a slowdown now as sales soften, it’s expected that they will be seeking more in financing for certain cash flow needs.

Industry Analysis

The used car industry represents a large portion of the vehicle importation industry in Jamaica with about 2/3 of all vehicles being imported being used. The majority of these vehicles originate from Japan and a few other Asian countries where there is a great resale market to third world countries like Jamaica where demand for cheap transport is high amidst weak public transport and housing systems. As highlighted by the Jamaica Used Car Dealers Association, there is a fledgling market space for this industry as seen by their 151 members (as of 2017) who operate in the space. This expansion of new dealers mainly came as a result of a surge in vehicle demand in Jamaica where there was an effective 100% in increase of cars imported, from 15,207 in 2014 to 31,231 in 2016. This demand was serviced by the commercial banks and other deposit taking institutions financing these vehicles through loans at interest rates ranging from 5 %– 9% with tenures (period of time) on these loans going as long as 84 or 96 months (7 or 8 years). With the capital (Kingston) seeing a greater increase in commercial activity but reduced housing space for the workers, many persons have opted to live in St. Catherine or other parishes and commute to work from further distances daily. Instead of relying on the route of commercial taxi’s and the Jamaica Urban Transit Company (JUTC), many persons chose to purchase a vehicle so that they could enjoy their commute without unnecessary fear of missing the last taxi. This also opened many commercial opportunities to persons who wished to use their vehicle as an asset to carry out their entrepreneurial activities. This can be highlighted by Jamaica’s declining unemployment rate which was at an all time low of 7.2% for October 2019, with many other persons engaging in their own personal hustle. Also, with car theft and motor vehicle accidents at all time highs, there is a space for insurance companies to replace vehicles for clients who are able to prove their claim that negligence wasn’t on their side. All of these numerous factors make the need to have a vehicle and sale of them a lucrative space for those who provide them to the growing market space.

However, there were some issues which made the opportunities for the numerous dealers harder. With the devaluation of the Jamaican Dollar (JMD) against the United States Dollar (USD), the cost to import vehicles was becoming more expensive and began to drive prices higher for vehicles brought in. This was also compounded by the limitations on the age of the vehicle that could be imported into the country which was 5 years. These combined factors can depress new sales for interested car buyers who would want a cheaper vehicle to purchase rather than take out a higher loan to finance it. A model which is 5 years older can fetch for a lower price rather than those which are within the 5 year stipulation. There was a recent adjustment in 2020 to this age limitation which saw the age for importation on most vehicles moved up by a significant amount. This opened up greater opportunities for those who wished to procure older models for clients.

A major problem with older vehicles comes down to reliability based on the age of the vehicle and remaining useful life left. As a result, there is a need to service them more frequently than newer vehicles which would possibly come with a warranty and free servicing. This problem was exasperated when the Trade Board noted numerous complaints about crashed and flooded cars being brought to the market with some speedometers being rolled back by as much as half of the distance traveled. The solution to this problem was inspection by an independent inspector at the country of origin along with a certificate to ensure that the vehicle being brought in wasn’t being obscured for its true state.

Market Analysis

Jetcon was listed on March 24, 2016 and delivered an astonishing return for investors considering it was one of the last set of companies to list on the junior market based on the fear that the provision would be extinguished by the government (PNP) at the time. The price rose from $2.25 (IPO price) to $6 by the end of the year. This period saw Jetcon traded for most of the year excluding 57 days where there was volume ranging from 500 units to more than 1 million during the period.

Within the first 20 days of January of 2017, the stock was up by 70% to $10.20. The price remained strong above $10 since that time and got an extra boost on the news of the 3:1 stock split. This even saw the stock have an astronomical intra-day trade of $26 the day before the ex-split date. With a new post split price of $5.66, the stock would now have an adjusted IPO price of $0.75. The stock rose to a peak closing price of $6.10 and leveled off for the rest of the year in the $4.50-$5.50 range. The closing price at the end of the year was $4.81 which still represented a gain of 140.50% for the entire year.

After the 2016 and 2017 runs, Jetcon’s stock price no longer saw massive gains as the stock began to decrease in price. The price closed at $3.04 and $1.69 for 2018 and 2019 respectively where the company posted slightly better results during the 2018 period. Since 2020 began, the stock has declined to a new low of $0.90 which is just slightly better than its IPO price. This left it with a PE ratio (price to earnings) of 9 times and a PB ratio (price to book) of 0.95 times which are much lower than prior ratios.

The free float of the company is less than 11% which represents the holdings of persons other than the top 10 shareholders, executives, directors and know unit trusts. This means that there is a heavy concentration of the stock among a select few with the remainder of the stock being traded by a few persons.

2019 Analysis

Jetcon recorded a 12% drop in revenues from their record high of $1.16 Billion to $1.02 Billion. This was accompanied by a 11% decline in cost of sales which left them with a gross profit of $135.7 Million. This left them with a gross profit margin of 13% compared with the 14% recorded in the prior year. Despite Jetcon attributing the fall in sales during the first quarter to the shift of consumers to purchase housing through mortgages, the company was able to maintain relatively stable sales throughout the rest of the year.

“In 2019, Jetcon had a $60.3 Million profit before taxation which was a 52% reduction against the $91.9 Million recorded in the 2018 period”

Expenses were marginally up by 7% to $76.5 Million which was mainly driven by greater administrative costs. This left Jetcon with $60.3 Million profit before taxation which was a 52% reduction against the $91.9 Million recorded in the 2018 period. Unlike in prior years where the company incurred a $60k minimum business tax (MBT) charge, this didn’t occur during the 2019 year as the government removed the MBT which was seen as non-conducive to existing and new business. The other comprehensive income of the firm went down by a marginal $11k as the investments stocks they held saw a decline in value compared with a $58.6k gain in the prior year.

The total asset base of the company went up by 21% to $680.7 Million with the bulk of this increase coming from current assets. Non-current assets went up by $54 Million to $135.8 Million with the major contributor of this increase coming from freehold property for the company. Current assets were up by $64 Million over the year which was mainly attributable to a significant increase in receivables as the other segments had flat changes. The company took on a new loan from JMMB Bank which saw its current liability segment increase to $29.3 Million versus nil in the prior year. The current liabilities experienced a sharp rise by the tune of 78% to $104 Million. This was mainly attributable to a rise in payables and a provision for the current portion of the long term loan. The bank overdraft facility was nil at the end of the year which left the company without any expensive debt going into the new year.

The cash provided by operating activities declined by $6 Million to $40.5 Million. The company spent $57.3 Million on its property, plant and equipment versus the $15.3 Million in the prior year. Cash from financing activities was positive during this period as the company took out a new loan. It should be noted that Jetcon paid out $17.5 Million in the year versus the $20.4 Million in the prior year which could be corresponded to the decline in profits.

Post Quarter 1 Analysis

On March 10, Jamaica recorded its first confirmed case of COVID19. Within the span of less than 3 weeks, the fallout from the slowdown in the economy began to be felt. This came in the form of numerous layoffs, delayed and cancelled transactions along with a dramatic decline in personal income. The government started to impose curfews and suspended many physical events which required large groups of people such as school and parties while imposing limits on those who could congregate in physical spaces to 20 (10 after a revision). These moves by the government resulted in there being a decreased demand to move around since most people were now at home with no immediate need to travel. All of these factors have reduced demand for both the new and used car industry.

Current Advantages During COVID19

With less staff needed on hand for operations, the firm will see a reduction in staff expenses as they contend with reduction in overall vehicle sales. This will prove to be an advantage for the firm as they enter an unknown period never yet seen in their history. With the company still in the first phase of the junior market, they will continue to enjoy the no income tax provision. This will allow for the company to survive the inevitable cash burn which will hurt other dealers.

Future Implications on Duration of COVID19

As long as COVID19 drags on in the local and global economy, the firm will struggle to get any new sales for the inventory they have on hand. The fundamental tenant (job) needed to secure a motor vehicle through a loan has been diminished amidst continued layoffs and salary cuts among the general population. There will be less jobs being created in the economy as remaining firms tighten their belts to remain viable during the current general economic conditions. With this uncertainty surrounding employment, the company with remaining car dealers will have no significant bargaining power over consumers who come to purchase a vehicle. This break down in financing will see some players in the industry inevitably cave under the pressure and close their doors permanently as they struggle to pay on going costs with operating cash flow at nil. With the current declines in remittance, tourism and current curfew like structure, it will take a while for normalcy to return the industry and overall economy. Jetcon themselves have a lease liability ($6 Million) due in May and have other statutory costs which must be paid to remain in operation. Also, persons no longer have a need to service their vehicles since they are using them a lot less now with the stay at home restrictions and curfews lowering the amount of travel carried out.

Until next time, stay safe, maintain your distance and Tan Ah Yuh Yard as we try to flatten the curve with COVID19. Enjoy the next article and keep reading past releases.

-DR

Note: This article is not intended to be financial advice or come off as a stated buy, hold or sell position against this company. I am not a licensed financial advisor and this article is intended to provide oversight and information on a listed JSE company.